Amid fluctuating industrial real estate conditions, the U.S. logistics sector has demonstrated notable resilience, according to the Q2 2023 U.S. Industrial Market Report released by Cushman & Wakefield. The market recorded robust activity with 29.9 million square feet of net absorption—nearly matching Q1's 30.3 million square feet—driven primarily by newly constructed logistics facilities.

Diverging Regional Performance

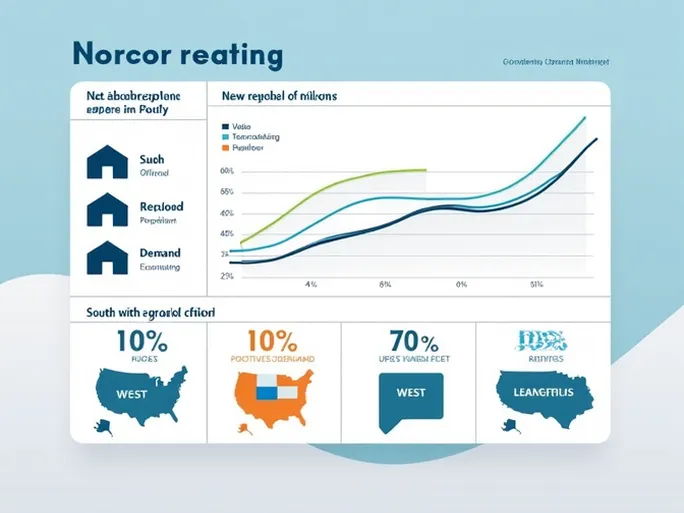

The report reveals that while national figures remained stable, regional disparities emerged. Western markets faced particular challenges, with overall net absorption declining by 2.3 million square feet. The Inland Empire and Los Angeles markets contracted by 1.8 million and 1.1 million square feet respectively, reflecting consolidation pressures and elevated vacancy rates.

Key findings from the report:

- Year-to-date leasing activity reached 309 million square feet, showing 0.3% annual growth but remaining 5.0% below pre-pandemic 2019 levels

- Q2 leasing activity totaled 157 million square feet (up 3.4% quarterly, down 1.0% annually), with seven major markets absorbing over 5 million square feet

- New supply declined to 71.5 million square feet (down 4.2% quarterly and 44.6% annually), with Southern and Western regions accounting for 68% of deliveries

- Build-to-suit projects increased to 30.4% of deliveries (from 16.8% in 2022), while speculative construction fell to 62.3%—the lowest since Q2 2020

- National vacancy rose modestly to 7.1%, though small warehouses (under 100,000 sq. ft.) maintained tighter vacancy at 4.4%

- Average rents reached $10.12 per square foot (up 0.9% quarterly, 2.6% annually), with small facilities commanding a 31% premium at $13.51

Market Dynamics Shifting

Jason Price, Cushman & Wakefield's Head of Logistics & Industrial Research for the Americas, attributed the demand rebound to multiple factors: "The improvement in Q2 demand stemmed partly from easing record-high tariffs and progress on international trade agreements. This created market clarity that boosted business confidence. Additionally, moderating rents allowed tenants to secure better terms than a year ago."

Price noted the supply pipeline has contracted significantly from 100 million square feet of new deliveries (80% speculative) in 2022. Vacancy increases have slowed to 20 basis points per quarter—half the 2023-2024 rate—indicating market stabilization.

When questioned about the 7.1% vacancy rate, Price contextualized: "This aligns with the 15-year pre-pandemic average. While elevated, it represents moderate health—especially since the increase comes primarily from new speculative supply rather than sublease or direct market space."

Future Outlook

Cushman & Wakefield projects new supply will continue outpacing absorption through most of 2025-2026, with the trend reversing in 2027 as demand catches up to reduced construction pipelines. The firm emphasizes that current conditions reflect a rebalancing rather than systemic weakness, with structural demand drivers like e-commerce and supply chain diversification supporting long-term fundamentals.