In today's globalized economy, international fund transfers have become commonplace, with cross-border remittances forming an integral part of daily financial activities. More than just moving money between locations, these transactions involve numerous technical details, including various banking codes and identifiers. Among these, the SWIFT/BIC code stands as a critical component ensuring accurate delivery of funds to their intended destinations.

Understanding SWIFT/BIC Codes

SWIFT (Society for Worldwide Interbank Financial Telecommunication) represents the international messaging protocol and network used by financial institutions. The BIC (Bank Identifier Code), often used interchangeably with SWIFT code, serves as a unique identifier for banks worldwide. These codes typically consist of 8 to 11 alphanumeric characters that convey specific information about the financial institution.

To illustrate their structure, let's examine the SWIFT/BIC code for Germany's ING-DIBA AG (a retail bank): INGDDEFFPFA

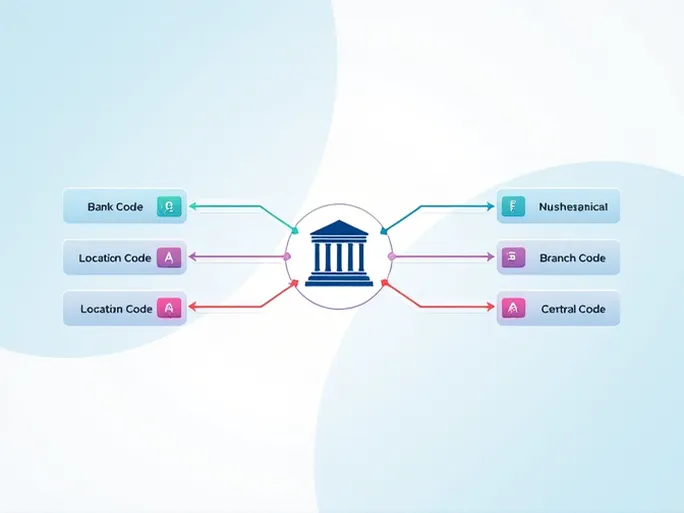

- Bank Code (INGD): The first four characters identify the specific bank (in this case, ING-DIBA AG).

- Country Code (DE): The following two letters indicate the country (Germany), using ISO standardized country codes.

- Location Code (FF): These characters specify the bank's city or region (Frankfurt, where ING-DIBA AG is headquartered).

- Branch Code (PFA): The final three characters identify a specific branch. Codes ending with 'XXX' typically denote a bank's head office.

The Critical Role in International Transfers

Accuracy in providing SWIFT/BIC codes proves essential for successful cross-border transactions. Once initiated, the receiving bank relies entirely on this code to process the transfer. Any errors in the code may result in misdirected funds, potentially causing significant delays or financial losses.

Financial institutions and money transfer services prominently display fields for SWIFT/BIC codes in their interfaces. Services like Western Union, PayPal, and international banking platforms all require this information to process overseas transactions. However, users must understand these codes to avoid costly mistakes.

Practical Considerations for Users

Modern digital banking solutions have simplified the process of locating SWIFT/BIC codes. Many financial institutions provide online search tools, while mobile banking applications increasingly incorporate verification features to confirm code accuracy during transaction setup.

Users should note that code formats may vary between banks and countries. Some institutions maintain different codes for specific account types or services. When preparing an international transfer, verifying all banking details—including the complete SWIFT/BIC code, account number, and recipient information—remains crucial for smooth transaction processing.

The Bigger Picture

As global financial activity continues expanding, understanding SWIFT/BIC codes has become increasingly important. These codes represent more than simple identifiers—they form a universal language within the international banking system, enabling secure and efficient transactions across borders.

For both individual users and business operators engaged in cross-border activities, familiarity with SWIFT/BIC codes constitutes an essential financial competency. Proper application of this knowledge helps prevent unnecessary fees, processing delays, and potential transaction errors in international money transfers.