In today's globalized financial landscape, the frequency of bank transfers has surged dramatically, particularly with the rise of cross-border transactions. Understanding the importance of SWIFT/BIC codes has never been more critical. These codes serve as the "passport" for financial transactions, ensuring both the security of funds and the speed of delivery. This article focuses on the SWIFT/BIC code for Bank of New Zealand, providing key insights to help you navigate international transfers seamlessly.

The Anatomy of a SWIFT/BIC Code

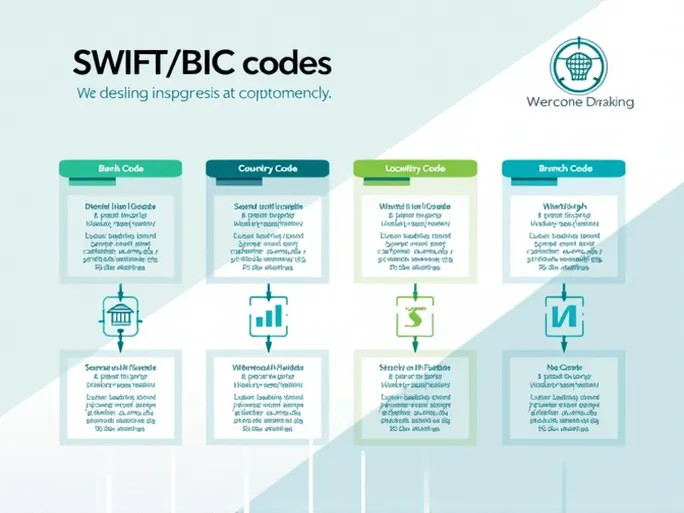

First, let’s break down the structure of a SWIFT/BIC code. Established by the Society for Worldwide Interbank Financial Telecommunication (SWIFT), this standardized system enables quick and accurate identification of financial institutions worldwide. A typical SWIFT/BIC code consists of 8 to 11 characters, structured as follows:

- Bank Code (BKNZ): Four letters representing the Bank of New Zealand. Each bank has a unique identifier.

- Country Code (NZ): Two letters indicating New Zealand as the bank’s home country.

- Location Code (22): Two digits specifying the bank’s headquarters or primary operational base.

- Branch Code (900): Three optional digits identifying a specific branch. A code ending with "XXX" typically denotes the bank’s headquarters.

For the Bank of New Zealand, the complete SWIFT/BIC code is BKNZNZ22900 .

- 8-digit SWIFT Code: BKNZNZ22

- Branch Code: 900

- Bank Name: Bank of New Zealand

- Address: 98 George Street, Dunedin, New Zealand

Key Considerations for Using SWIFT/BIC Codes

Accuracy is paramount when using SWIFT/BIC codes. Errors can delay transactions or even result in lost funds. Here are critical factors to verify:

- Bank Name: Confirm the SWIFT code matches the recipient’s bank name exactly.

- Branch Details: If using a branch-specific code, ensure it aligns with the recipient’s branch.

- Country Code: Verify the country code corresponds to the recipient’s bank location, especially for multinational banks.

Selecting an International Transfer Provider

Choosing the right service provider can significantly impact the cost and speed of international transfers. While traditional banks remain an option, specialized platforms often offer superior exchange rates and lower fees. Key features to look for include:

- Competitive Exchange Rates: Providers offering near-interbank rates can save substantial amounts, especially for large transfers.

- Transparent Fees: Clear, upfront pricing avoids hidden charges.

- Speed: Many services now process transfers within one business day, ensuring timely delivery.

Practical Applications of SWIFT/BIC Codes

SWIFT/BIC codes facilitate a wide range of international financial activities:

- Personal Transfers: Sending money to family or friends abroad.

- Business Transactions: Paying suppliers, receiving payments from overseas clients, or managing multinational payroll.

- Real Estate: Securing cross-border property purchases with timely fund transfers.

Conclusion

Mastering the use of SWIFT/BIC codes is essential for anyone engaged in international banking. By ensuring the accuracy of these codes and selecting efficient transfer services, individuals and businesses can optimize their cross-border financial operations. Whether for personal remittances or corporate transactions, understanding these details safeguards both the security and efficiency of global money movement.