In today's global financial system, SWIFT/BIC codes serve as the backbone of international money transfers and interbank communication. These standardized identifiers enable seamless cross-border transactions while maintaining security and efficiency. The case of ARAB BANK PLC, with its SWIFT/BIC code ARABPS22060, illustrates both the complexity and importance of this system in modern finance.

Anatomy of a SWIFT/BIC Code

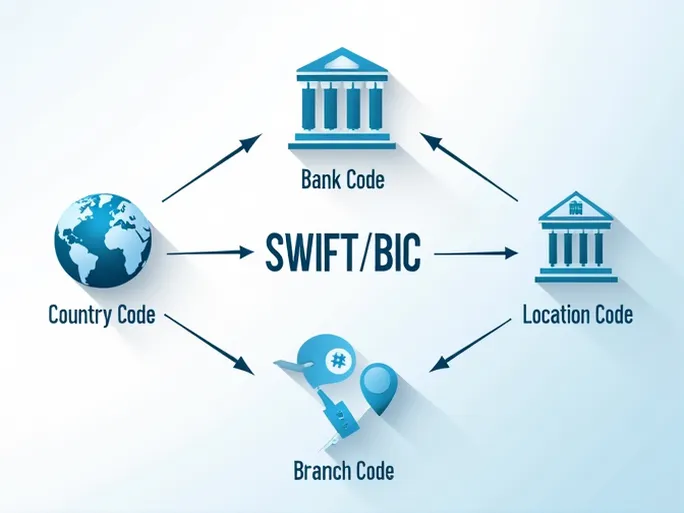

The Society for Worldwide Interbank Financial Telecommunication/Bank Identifier Code (SWIFT/BIC) consists of 8 to 11 characters, each segment carrying specific identification purposes:

- Bank Code (ARAB): The first four characters uniquely identify the financial institution. In this case, "ARAB" designates ARAB BANK PLC, preventing confusion with similarly named entities.

- Country Code (PS): The subsequent two characters indicate the bank's registered country. "PS" represents Palestine, crucial for compliance with international financial regulations and jurisdictional requirements.

- Location Code (22): These two digits specify the bank's operational headquarters, assigned according to internal banking protocols to ensure transaction accuracy.

- Branch Code (060): The final three characters identify specific branches. An "XXX" suffix denotes the institution's primary office, while other combinations direct transactions to precise processing centers.

The complete SWIFT/BIC code ARABPS22060 demonstrates how each component collaboratively ensures precise routing of international payments.

Operational Significance in Global Transactions

As economic globalization intensifies, the proper use of SWIFT codes becomes increasingly vital. Errors in code entry can lead to delayed settlements, failed transactions, or financial losses. Key verification steps include:

- Confirming exact bank name matching with recipient records

- Validating specific branch codes for corporate transactions

- Ensuring country codes align with the beneficiary bank's jurisdiction

Navigating Cross-Border Payment Challenges

Despite SWIFT's standardized framework, international transfers face multiple obstacles including regulatory variations, exchange rate fluctuations, and intermediary bank charges. Mitigation strategies involve:

- Researching destination country financial regulations and market conditions

- Monitoring foreign exchange trends for optimal transfer timing

- Utilizing transaction tracking technologies for real-time monitoring

Financial institutions continue enhancing SWIFT-related services to address these complexities, implementing advanced verification protocols and automated routing solutions.