In today's increasingly globalized financial landscape, understanding how to effectively conduct international money transfers has become essential. When sending money across borders, IBAN and SWIFT codes are the two most commonly used banking identifiers. While they serve different functions, both are crucial for ensuring your funds reach their intended destination smoothly. This article provides a detailed explanation of IBAN and SWIFT codes, their functions, key differences, and practical usage tips to help you avoid unnecessary delays and errors in international transactions.

What Is an IBAN?

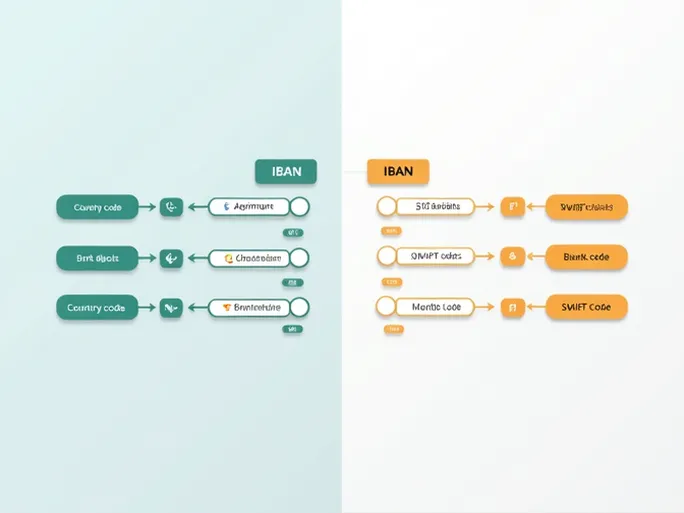

The International Bank Account Number (IBAN) is used to precisely identify a specific bank account when receiving funds in international transfers. Widely adopted in Europe, the Middle East, and several other regions, the IBAN system was designed to reduce transaction errors and improve processing efficiency.

Structure of an IBAN

An IBAN consists of up to 34 alphanumeric characters, structured as follows:

- Country Code (CC): Two letters representing the destination country

- Check Digits (XX): Two numbers used for validation

- Bank Identifier (BBBB): Varies by country, identifies the specific bank

- Account Number (AAAA...): The recipient's unique account identifier

What Is a SWIFT Code?

The SWIFT code (Society for Worldwide Interbank Financial Telecommunication code) serves as a unique identifier for financial institutions in the international payment network. Its primary function is to provide a precise "bank address" for cross-border transactions, ensuring funds are routed to the correct institution.

Structure of a SWIFT Code

A SWIFT code typically contains 8 to 11 characters with the following components:

- Bank Code (AAAA): Four letters identifying the specific bank

- Country Code (BB): Two letters representing the country

- Location Code (CC): Two characters identifying the city or region

- Branch Code (DDD): Optional three-character identifier for specific branches

Key Differences Between IBAN and SWIFT

While both IBAN and SWIFT codes play vital roles in international money transfers, they differ significantly in function and application. The following table summarizes their key distinctions:

| Feature | IBAN | SWIFT |

|---|---|---|

| Definition | International Bank Account Number | Society for Worldwide Interbank Financial Telecommunication code |

| Primary Function | Identifies a specific bank account | Identifies financial institutions globally |

| Usage | Account verification | Routing international payments |

| Format | Up to 34 characters | 8-11 characters |

| Governing Body | National regulators with international standards | SWIFT organization |

| Geographic Use | Primarily Europe, Middle East, and some other regions | Worldwide |

Choosing the Right Code for Your Transfer

When initiating an international money transfer, selecting the appropriate code(s) depends on the destination. Consider these guidelines:

- Transfers to Europe, the Middle East, or the Caribbean: Typically require an IBAN and may need a SWIFT code

- Transfers to the U.S., Canada, Australia, or Asia: Usually require only a SWIFT code

- Some countries require both: SWIFT ensures funds reach the correct bank, while IBAN verifies the account

Practical Transfer Examples

To better understand application of these codes, consider these common scenarios:

- Sending money to a student in Germany: Requires the recipient's IBAN and typically the bank's SWIFT code

- Transferring funds to a business partner in Japan: Only the SWIFT code is needed as Japan doesn't use IBAN

- Sending money to family in the UK: Both IBAN and SWIFT codes are typically required

When uncertain about required information, always verify details with the recipient or their bank. Understanding IBAN and SWIFT codes is fundamental for efficient international money transfers, helping prevent financial losses while ensuring a smooth cross-border banking experience.