When sending money across borders, incorrect bank details can lead to delays or even lost funds. One of the most common causes of such issues is misunderstanding or misusing SWIFT/BIC codes. Properly identifying and applying these codes ensures smoother and faster transactions.

A SWIFT/BIC code is a crucial banking identifier, consisting of 8 to 11 alphanumeric characters, used globally for secure interbank transfers. For example, breaking down the code RABONL2UPBO reveals its structure and significance:

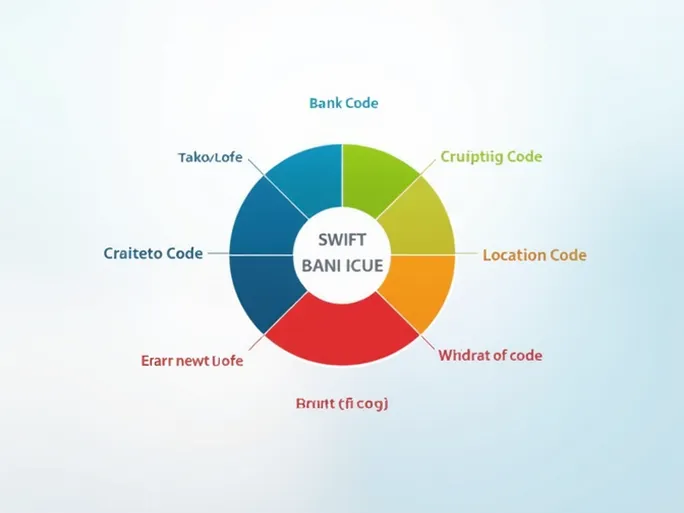

Anatomy of a SWIFT/BIC Code

- Bank Code (RABO): The first four letters represent the bank's name—here, "RABO" stands for Rabobank.

- Country Code (NL): The next two letters indicate the country where the bank is located ("NL" for the Netherlands).

- Location Code (2U): These characters pinpoint the bank's headquarters or primary branch, ensuring accuracy in routing.

- Branch Code (PBO): The final three digits specify a particular branch. If the code ends with "XXX," it denotes the bank's main office.

Avoiding Common Pitfalls

Using an incorrect SWIFT/BIC code can result in delayed transactions, misdirected funds, or additional complications. To prevent these issues, consider the following precautions:

- Verify Bank Details: Confirm that the recipient bank's name matches the provided BIC.

- Check Branch Specifics: Ensure the SWIFT code corresponds to the recipient's branch, not just the bank's general code.

- Validate Country Information: Cross-check that the SWIFT code aligns with the recipient bank's country.

By paying close attention to these details, senders can minimize risks and ensure their international transfers proceed without complications.