In today's globalized financial landscape, navigating international transactions requires understanding key banking identifiers like SWIFT codes. Whether processing overseas remittances or conducting international business, proper use of SWIFT/BIC codes proves critical for successful cross-border transfers.

DUTCH-BANGLA BANK PLC., a prominent financial institution based in Bangladesh, utilizes the SWIFT/BIC code DBBLBDDH106 . The bank's headquarters are located at 45 (OLD) S.M. MALEH ROAD, NARAYANGANJ, DHAKA, 1400. This comprehensive guide explores SWIFT code fundamentals, their structural composition, and operational significance in global banking transactions.

The Critical Role of SWIFT Codes

SWIFT codes (alternatively called BIC codes) represent standardized identifiers developed by the Society for Worldwide Interbank Financial Telecommunication. These unique alphanumeric sequences serve as global banking addresses, facilitating secure and efficient international money transfers across 200+ countries.

Functioning similarly to postal codes, SWIFT identifiers ensure accurate routing of funds between financial institutions. When transferring money to DUTCH-BANGLA BANK PLC., using the correct DBBLBDDH106 code prevents potential transfer failures, misdirected funds, or fraudulent activities. Precise SWIFT code implementation remains essential for both individual and corporate cross-border transactions.

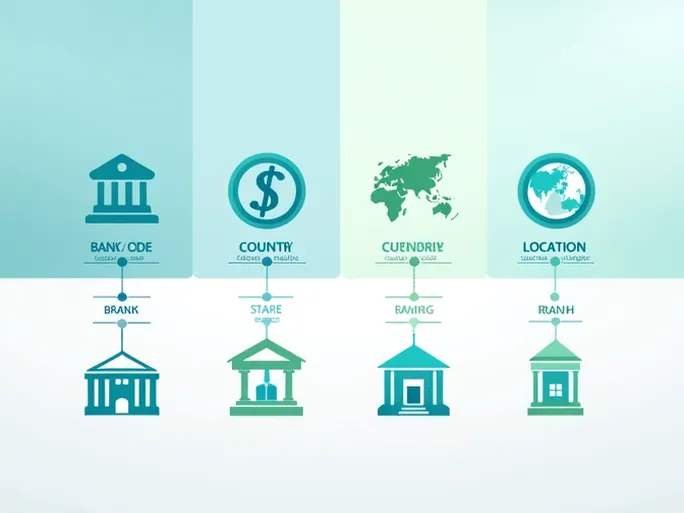

Decoding SWIFT/BIC Structure

SWIFT codes contain 8-11 characters with specific informational components:

- First 4 letters: Bank identifier (DBBL for DUTCH-BANGLA BANK PLC.)

- Next 2 letters: Country code (BD for Bangladesh)

- Following 2 characters: Location identifier (DH for Dhaka)

- Optional final 3 digits: Branch-specific code (106 denotes a particular branch)

International Transfer Protocol

1. Bank Information Verification

Confirm the recipient bank's exact legal name matches official records. Discrepancies in bank naming conventions can cause transfer rejections. When initiating first-time transactions with DUTCH-BANGLA BANK PLC., cross-verify details through official banking channels.

2. Branch-Specific Details

Utilize branch-specific SWIFT codes when available. Different branches within the same banking network may employ distinct identifiers. The inclusion of "106" in DBBLBDDH106 specifies routing to a particular DUTCH-BANGLA BANK PLC. branch.

3. Country Code Validation

Verify the SWIFT code's embedded country designation matches the destination nation. Incorrect country codes represent a common source of international transfer errors.

4. Transaction Submission

Complete transfer forms with precise beneficiary details including full name, physical address, bank information, SWIFT code, and transfer amount. Conduct final verification before submission to prevent processing delays.

Practical Applications of SWIFT Codes

SWIFT codes facilitate diverse financial operations beyond personal remittances, including:

- International trade settlements

- Corporate treasury operations

- Foreign direct investments

- Cross-border payroll processing

- Import/export financing

Major payment platforms including Western Union and PayPal mandate SWIFT codes for international fund transfers. Businesses conducting high-value transactions particularly benefit from understanding SWIFT protocols to mitigate financial risks.

Frequently Asked Questions

What happens with incorrect SWIFT codes?

Erroneous SWIFT codes may route funds to wrong accounts or cause complete transfer failure. Recovery processes typically involve lengthy bank investigations and potential financial losses.

Where to find SWIFT codes?

Financial institutions generally publish SWIFT codes on official websites and banking documentation. Customers may also obtain codes through direct bank inquiries.

Do all banks use SWIFT codes?

While most international banks participate in the SWIFT network, some regional institutions utilize alternative transfer systems. These cases require specialized remittance services.

Security Considerations

When conducting international transfers, safeguard sensitive banking information including SWIFT codes and account details. Verify recipient credibility before initiating transactions and maintain awareness of evolving financial regulations affecting cross-border payments.